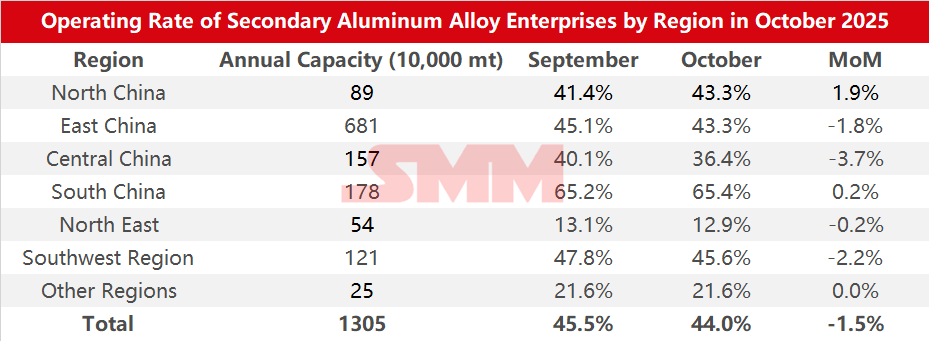

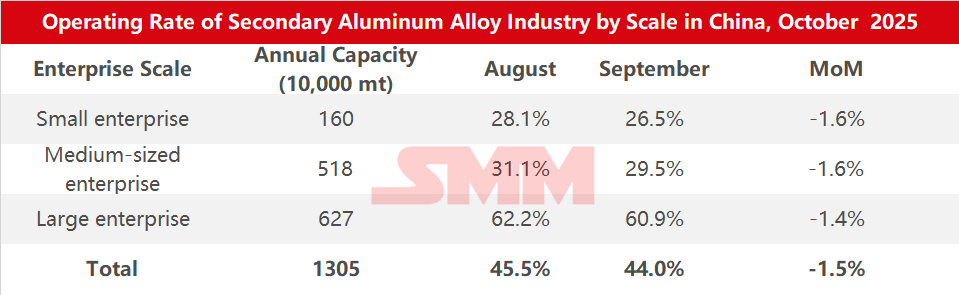

Survey Data on Operating Rates of Secondary Aluminum Alloy Enterprises by Region and Scale in October 2025:

According to the SMM survey, the operating rate of the secondary aluminum industry in October 2025 fell 1.5 percentage points MoM to 44.0%, but rose 2.2 percentage points YoY.

In October, affected by multiple factors, the overall industry operating rate was under pressure. The main constraints included:

(1) Holiday shutdown impact: Aluminum liquid direct supply enterprises maintained continuous production, but mostly adopted shift systems and appropriately reduced load operations; some enterprises suspended production for about three days. The overlapping Mid-Autumn Festival and National Day holidays led to extended holidays for downstream enterprises, causing orders for secondary aluminum enterprises to contract MoM.

(2) Raw material supply gap: The tight supply of domestic aluminum scrap in October remained unchanged, with the difficulty of recycling aluminum tense scrap being particularly prominent. Meanwhile, limited supplementary supply from imported aluminum scrap due to persistent price inversions left enterprises facing procurement difficulties. Raw material inventories continued to be consumed, but restocking was hindered.

(3) Cost squeeze pressure: Affected by the continued tight supply of aluminum scrap, traders actively followed price increases, driving the cost per metric ton of aluminum scrap up sharply by 304 yuan MoM in October. Simultaneously, copper prices continued to hit record highs, coupled with rising silicon prices, squeezing the raw material costs for secondary aluminum plants. As cost increases were too rapid, the theoretical profit margin for the industry was compressed, even leading to losses, forcing enterprises to cut production.

(4) Policy disruptions: Some enterprises in Henan, Jiangxi, and other regions continued production cuts or suspensions due to uncertainty regarding tax rebate policies, focusing mainly on digesting finished product inventories, with production tending to be conservative.

(5) Impact of environmental protection-driven production restrictions: Environmental protection-related controls initiated at month-end in Hebei and other areas caused disruptions to local production and transportation, but the overall impact was controllable.

Entering November, as the holiday factor subsides and year-end demand for pushing annual targets is released in the end-use market, orders and operating rates for secondary aluminum plants are expected to receive phased support. However, the industry still faces multiple challenges: on one hand, raw material supply shortages, regional environmental protection-driven production restrictions, and policy uncertainties continue to hinder capacity release; on the other hand, the rapid rise in aluminum prices in November led to a significant decline in downstream purchase willingness, with insufficient momentum for rushing to buy amid continuous price rises, resulting in a contraction of secondary aluminum orders and further constraining the upside room for the operating rate. Overall, the industry's operating rate in November is expected to show a slight MoM improvement but appear weak YoY.